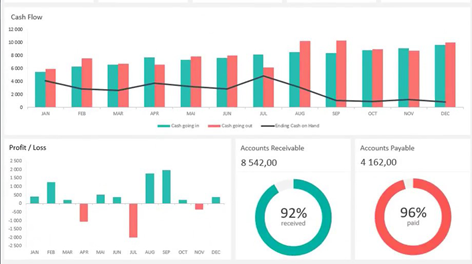

Cash flow management is a process of tracking the movement of cash in and out of your business. This helps you predict how much money will be available to your business in the future. It also helps you identify how much money your business needs to cover debts, like paying staff and suppliers.

Cash flow is the term used to describe changes in how much money your business has from one point to another. Cash flow management is keeping track of this flow and analysing any changes to it. This helps you spot trends, prepare for the future, and tackle any problems with your cash flow.

It pays to practice cash flow management often to make sure your business has enough money to keep running.

Contact us to see how we can help you manage your cash flow on 020 8343 3523

Managing Interest Rate Risk

There are different ways to deal with interest rate exposure:

Interest Rate Mix

A company may decide to have a mix of fixed and variable rate debt to reduce the effects of unanticipated rate movements.

Forward Rate Agreement (FRA)

Some risk exposure could be eliminated by entering into a forward rate agreement with the bank. This would lock the company into borrowing at a future date at an agreed interest rate. Only the difference between the agreed interest that would be paid at the forward rate and the actual loan interest is transferred.

Interest Rate ‘Cap’

It is possible to ‘cap’ the interest rate to remove the risk of a rate rise. If the cap is set at say 7%, an upper limit is placed on the rate the company pays for borrowing a specific sum. Unlike the FRA, if the rate falls, the company does not have to compensate the bank.

Interest Rate Futures

These contracts enable large interest rate exposures to be hedged using relatively small outlays. They are similar in effect to FRAs, except that the terms, the amounts and the periods are standardised.

Interest Rate Options

Also termed interest rate guarantees, these contracts grant the buyer the right, but not the obligation, to deal at a specific interest rate at some future date. For example, if a company is borrowing money, then the interest rate option will protect the borrower from interest rate rises. However, if interest rates fall, then the borrower can benefit from the reduction in interest rates. The borrower will need to be willing to pay the premium for the interest option.

Interest Rate ‘Swaps’

These occur where a company (usually large companies) with predominantly variable rate debt, worried about a rise in rates, ‘swaps’ or matches its debt with a company with predominantly fixed-rate debt concerned that rates may fall. A bank usually acts as intermediary in the process, but it can be through direct negotiations with another company. Each borrower will still remain responsible for the original loan obligations incurred. Typically, firms continue to pay the interest on their own loan and then, at the end of the agreed period, a cash adjustment will be made between the two parties to the swap agreement. Interest rate swaps can also involve exchanges in different currencies.

Multiple Choice Accountancy. © Terms. All rights reserved

Multiple Choice Accountancy is a fast growing accountancy practice.

Your Business Success is Our Mission!

Registered address Colton House, Princes Avenue, Finchley, London. N3 2DB

Audit & Assurance Services:

Statutory Audit

Internal Audit

Assurance

Cash Flow Management

Risk Advisory

Service Charge Audit